Weekly market intelligence on commodities, geopolitics, deals and financing trends across Africa's extractive minerals sector.

The most dramatic week in the Iran peace process since Versailles. Trump declared the memorandum of understanding 'over' on Wednesday 8 July after renewed US-Iran military strikes over the weekend. Oil surged more than 5% in a single session and global stocks tumbled. By Thursday Iran had reached out seeking a deal and by Friday both sides were apparently back in talks — leaving markets in a state of deep uncertainty about where the 60-day framework actually stands. Gold ended the week down 1.5% at around $4,100, reflecting the renewed rate hike fears that follow any oil price surge. Kamoa-Kakula reported 64,328 tonnes of copper in Q2 — strong output despite the acid headwinds tracked all year. India's silver import restrictions are now creating real shortages, with premiums at a six-month high. And a theme that has been building across this newsletter for months reached a new level this week: Burkina Faso awarded a state mining permit to its own company to build and operate a gold mine — no foreign partner, no co-ownership structure, state-owned and state-operated from day one.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,635 – 1,695 | Continued weakness |

| ZAR — South African Rand | ~18.3 – 19.1 | Volatile; gold pressure and oil spike both headwinds |

| GHS — Ghanaian Cedi | ~15.0 – 16.0 | Weak |

| ZMW — Zambian Kwacha | ~25.3 – 26.5 | Mild softening; oil spike reversal temporary |

| EUR — Euro | ~1.07 – 1.10 | Steady |

| GBP — British Pound | ~1.30 – 1.33 | Broadly stable |

The oil surge on Wednesday pushed the dollar higher and weighed on African currencies with significant import bills. ZAR was caught between gold price pressure and oil cost pressure simultaneously. The partial recovery in both oil and gold on Thursday and Friday provided limited relief. Sources: LME, ICE, Refinitiv, CME, Fastmarkets.

Iran deal — Trump declared it 'over', then both sides were back in talks by Friday. The most significant single development of the week. Renewed military strikes over the weekend preceded Trump's Wednesday declaration that the MoU was finished. Oil surged 5%. Gold fell. By Thursday Iran reached out seeking a deal. By Friday talks were apparently back on. The deal is not a binary event — it keeps oscillating without settling.

Federal Reserve July 29 meeting — still likely a hold. Despite renewed Iran tensions pushing oil higher, markets are pricing just a 25% probability of a rate hike at July 29. The September meeting is where the market sees the greater risk, with probability near 60% if oil stays elevated through the summer.

Allied-Zijin — deadline 29 July, no NDRC announcement. Outside date now two weeks away. No Chinese regulatory approval confirmed. The 21% share price discount to the offer price persists.

Diamonds for Development Fund — still no board announcement. Fifth consecutive week without independent director appointments. The fund remains in its establishment phase. This is becoming a meaningful delay.

Kamoa-Kakula Q2 output confirmed at 64,328 tonnes. Strong result despite the acid headwinds tracked across the past three editions. Improved mining rates and processing throughput both cited as drivers.

Ivanhoe Mines reported that Kamoa-Kakula, its flagship copper operation in the DRC, produced 64,328 tonnes of copper in Q2 2026 — a result that carries real weight given acid prices at the site rose from $467 per tonne in Q1 to $725 per tonne for June delivery, a 55% increase in three months. Input cost headwinds of that scale typically compress production volumes, so the Q2 number is an operational resilience signal in its own right. Separately, sovereign participation reached a new level this week: Burkina Faso's military government awarded an industrial mining permit to its own state-owned company, SOPAMIB, for the Bouboulou gold project in Yako commune — no foreign partner, no joint venture, no co-ownership structure. The project contains an estimated 10.77 million tonnes of ore and is expected to produce 7.27 tonnes of gold over a 15-year mine life, requiring roughly $56 million in investment that has not yet been funded. Tanzania's central bank separately revealed it has bought 28 tonnes of gold over 18 months to strengthen its own currency. And in Senegal, Canadian processor Dynacor began commissioning its Galam plant in Kedougou — a facility designed to formalise artisanal gold production by buying ore directly from small-scale miners, process up to 50 tonnes a day, with first gold pour expected in August.

Everything tracked in this newsletter since April traces back to one variable: whether the US and Iran reach a final, verified, lasting agreement. This week showed how fast that variable can swing — a deal declared dead and apparently revived within 72 hours. Underneath that volatility, Kamoa-Kakula's Q2 output proves African copper assets can absorb serious input cost shocks, and Burkina Faso's SOPAMIB permit confirms that sovereign participation is now pushing past co-ownership into full state ownership. The question for AEMBank is no longer whether these trends are real — it is what financing instruments meet them where they are.

A question that sits underneath every story in this edition is one that any bank active in African mining needs to be thinking about. As African governments move from licensing and taxing foreign operators toward owning and operating their own mines, what does that mean for how international finance institutions structure their involvement? Three questions are worth working through. First — what financing instruments work for state-owned mining entities? Sovereign-backed facilities, project finance with government guarantee, or blended instruments combining concessional and commercial tranches each carry different risk profiles; the Lobito Corridor's infrastructure financing model is one reference point for how this can work at scale. Second — how do you assess governance when the operator and regulator are the same entity? Board independence, ring-fenced project accounts, environmental covenants and independent technical advisors are the tools available. Third — sovereign payment timing risk. A government that mandates ambitious policies but is slow to honour its financial obligations to existing operators is the cautionary case; currency retention mechanisms, payment waterfall structures and escrow arrangements are becoming standard requirements for any credible African mining finance framework.

Three themes stand out this week. The Iran deal oscillation requires explicit scenario maintenance in every African mining credit model — Trump's Wednesday declaration and Friday reversal within 72 hours is the clearest evidence yet that a settled base case cannot be assumed. AEMBank should maintain two live scenarios for every deal with commodity, fuel or acid cost exposure: a deal-holds scenario with oil at $69 to $75 and a deal-collapses scenario with oil back above $90. Sovereign participation financing is becoming a core product requirement, not an edge case — Burkina Faso's SOPAMIB permit, Ghana's Tarkwa review, Zimbabwe's co-ownership mandate and Tanzania's domestic gold purchases all confirm that African governments are asserting more direct control across multiple jurisdictions simultaneously, and AEMBank needs financing instruments specifically designed for state-owned mining entities. Artisanal mining formalisation is an underexplored segment of AEMBank's addressable market — Dynacor's Senegal plant sits at the intersection of beneficiation, governance and financial inclusion, though the financing gap is real given Dynacor's limited balance sheet.

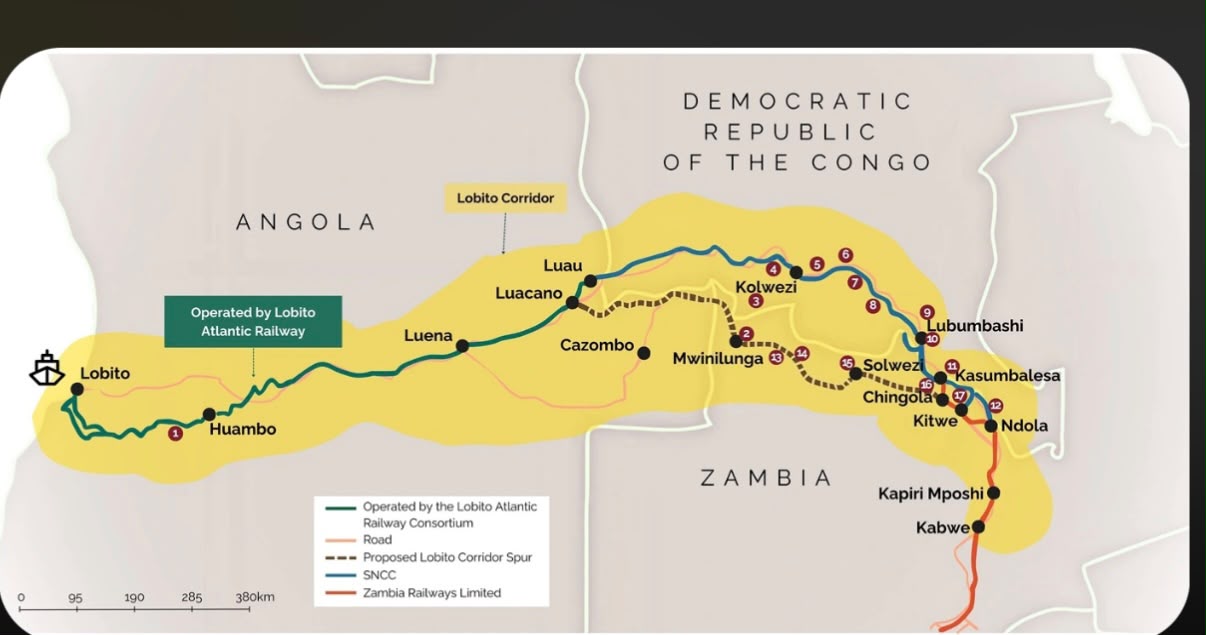

Gold broke above $4,100 on Thursday and was climbing toward $4,200 by Friday after the June US jobs report came in at 57,000 — less than half the 115,000 forecast — sharply reducing the probability of a Federal Reserve rate hike at its July 29 meeting from 63% six weeks ago to less than 30% today. Oil settled near $69 per barrel, the lowest since before the Iran war began in February, as Hormuz shipping continues to normalise and Saudi Arabia restores 90% of pre-war export volumes. The Lobito Corridor railway — 1,300 kilometres of rehabilitated rail linking the Port of Lobito in Angola to the DRC Copperbelt — achieved $753 million financial close on Friday, with $553 million from the US government and $200 million from the Development Bank of Southern Africa. South32 signed a binding agreement to sell its South African aluminium assets to Alcoa for up to $5.6 billion. The DRC withdrew unused cobalt export quotas and signed a diamond processing deal with Swiss firm ADEX — two minerals, same week, same direction. And mining cost pressures in South Africa accelerated sharply in May as energy costs surged, with the Minerals Council warning that relief will be gradual even as the global energy shock begins to unwind.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,630 – 1,690 | Continued weakness |

| ZAR — South African Rand | ~18.0 – 18.8 | Firming; lower oil import bill and gold recovery |

| GHS — Ghanaian Cedi | ~15.0 – 16.0 | Weak |

| ZMW — Zambian Kwacha | ~25.0 – 26.2 | Stable to firming on lower fuel costs |

| EUR — Euro | ~1.08 – 1.12 | Firmer on lower oil |

| GBP — British Pound | ~1.31 – 1.35 | Broadly stable |

The US dollar softened on Friday following the weak jobs report as rate hike expectations declined sharply. ZAR and ZMW both benefited from the combination of lower oil import costs and recovering precious metals prices — the first week in which both tailwinds have been visible simultaneously. Sources: LME, ICE, Refinitiv, CME, Fastmarkets.

Switzerland talks — rescheduled and concluded positively. The Friday 19 June postponement flagged in the prior edition resolved quickly. The main Switzerland talks took place on 21–22 June at Lake Lucerne and concluded positively — Iran agreed to IAEA nuclear inspector access and both sides agreed on a roadmap. Talks then moved to Doha this week, mediated by Qatar and Pakistan. Qatar confirmed positive progress on 1 July. The next round is paused briefly for Iran's state funeral following the death of the former Supreme Leader in the February strikes. Talks resume after.

Oil below $70 — Hormuz normalising on schedule. Brent at $69 — the IEA's two-to-three month normalisation timeline is tracking. Saudi Arabia at 90% of pre-war volumes. UAE fully restored. The lagged relief to African mining input costs — diesel and acid — is now within a one-to-two month window.

Cobre Panama — audit passed, restart still pending. Panama's government has not yet confirmed a formal restart timeline. The 88% audit score keeps the option open but political risk around public sentiment remains the primary constraint.

Diamonds for Development Fund — no board news for third consecutive week. Adesina is in office. Independent director appointments remain the outstanding milestone.

Allied-Zijin — outside date 29 July approaching. No NDRC announcement. The 21% share price discount to the C$44 offer price has not narrowed, signalling continued institutional scepticism about Chinese approval ahead of the deadline.

South African mining input costs accelerated sharply in May. The Minerals Council Mining Cost Index shows petroleum products up 15.3% month-on-month, chemicals up 11.5%, and overall costs up 2.3% in May alone. Domestic utility tariff increases now in force from mid-June mean cost relief will lag the oil price fall by at least one quarter, independent of the Hormuz resolution.

Gold broke above $4,100 on Thursday 3 July after the June US nonfarm payroll report delivered a sharp downside surprise — 57,000 jobs added against a consensus forecast of 115,000, the weakest monthly gain since February. A weak jobs number signals economic softening, which means inflation is likely to ease, which removes the Fed's justification for raising rates — the CME FedWatch tool now shows less than a 30% probability of a hike at the 29 July meeting, down from 63% six weeks ago. Separately, the Lobito Corridor railway achieved $753 million financial close, backed by $553 million from the US DFC and $200 million from the Development Bank of Southern Africa. The 1,300-kilometre rehabilitated line links the Port of Lobito to the DRC Copperbelt, cutting transit time for cobalt and copper from 45 days to under 8 and cost by 30% — a direct extension of the US strategy of routing African critical minerals into Western supply chains through infrastructure rather than extraction. South32 agreed to sell its Hillside aluminium smelter in KwaZulu-Natal to Alcoa for up to $5.6 billion, a live valuation benchmark for South African processing assets. And the DRC withdrew unused cobalt export quotas while simultaneously signing a diamond processing joint venture with Swiss firm ADEX — two separate minerals, the same week, pointing in the same direction of Kinshasa actively managing its mineral portfolio rather than passively hosting extraction.

The rate-easing path and the Hormuz normalisation path are now both confirmed in market pricing, not just diplomatic signals — gold above $4,100 and oil near $69 tell the same story from two directions. Meanwhile the Lobito Corridor's financial close is the clearest evidence yet that Western capital is building permanent infrastructure into the Copperbelt, not just signing MoUs. And the DRC's simultaneous moves on cobalt and diamonds confirm that sovereign participation in African minerals is now a standing policy posture, not an episodic reaction — a theme AEMBank should treat as the new baseline for every transaction, not an emerging risk.

A question that has appeared in different forms across nearly every edition of this newsletter since April is crystallising this week into something that deserves to be named directly: when a foreign company mines African resources, how much of the value actually stays in Africa — and are African governments finally building the structures to change that? Ghana let the lease on Gold Fields' Damang mine expire and ran a restricted tender open only to Ghanaian companies, successfully transferring a working mine to a local operator, and is now weighing the same decision for the much larger Tarkwa mine ahead of its April 2027 lease expiry. Zimbabwe mandated state co-ownership across 14 critical minerals with an immediate raw export ban, yet simultaneously owes its platinum producers $228 million in unpaid export earnings — exposing the gap between policy ambition and fiscal capacity. Botswana renegotiated its entire De Beers relationship from a position of leverage. This week's DRC stories — cobalt quota withdrawal and the ADEX diamond JV — add two more data points in the same direction: Kinshasa is managing its mineral portfolio as an active sovereign instrument, not a passive resource base. For AEMBank, the practical implication is not abstract — lease renewal risk, state participation requirements and sovereign payment timing are no longer edge cases; they are the new baseline for any transaction involving a foreign operator in an African jurisdiction.

Three themes stand out this week. The Lobito Corridor financial close is a direct benchmark for AEMBank infrastructure financing — the $753 million deal was structured by AFC and Eaglestone using a blended architecture of US DFC concessional lending and DBSA senior debt, directly challenging the conventional view that African infrastructure deals of this complexity cannot be financed domestically. South African cost pressure requires an explicit Q3 overlay on all SA mining models — the Minerals Council's May data (15.3% fuel cost increase, 11.5% chemicals increase, 2.3% overall index rise) combined with utility tariff increases now in force mean cost assumptions cannot assume immediate normalisation simply because oil has fallen. Sovereign participation risk should be formally incorporated as a first-order credit criterion — the convergence of DRC, Ghana, Zimbabwe and Botswana actions confirms that who controls an asset, and on what terms, is now a primary credit consideration across every major African mining jurisdiction.

Gold surged to $4,887 an ounce this week — its highest level since mid-March — after Iran declared the Strait of Hormuz fully open to commercial traffic during the ceasefire period. Bullion has now recovered more than half of all its 2026 losses in under two weeks. Silver surged over 5% to a five-week high above $83. Oil eased to around $80 a barrel, down sharply from the April peak above $120, though the IEA cautioned that full supply normalisation remains a two-to-three-month story given the scale of the shipping backlog. Heraeus published an analysis of the World Gold Council survey showing 75% of central banks now classify gold as a strategic asset rather than a historical legacy holding — up from just 44% a year ago. And First Quantum's shuttered Cobre Panama copper mine passed an environmental audit, opening the door to a possible restart of one of the world's largest copper assets. The week closed on a note of caution: formal talks scheduled in Switzerland were abruptly postponed on Friday, a reminder that the interim deal remains fragile.

Gold and silver both posted their strongest weekly gains in over a month, fully reversing the post-FOMC pullback from the prior edition. Brent remains roughly $20 above where it started the year despite the sharp fall from its April peak — the IEA notes operational and political constraints, including prolonged demining and unresolved transit arrangements, leave downside risks to the outlook. Sources: LME, ICE, Refinitiv, CME, Fastmarkets.

Strait of Hormuz — commercial traffic resumed. Iran declared the Strait fully open to commercial vessels during the ceasefire period this week, the most concrete physical signal yet that the MoU is being implemented in practice, not just on paper. Gold and silver responded immediately. The IEA's June Oil Market Report confirms the direction but cautions that full shipping normalisation, given roughly 500 stranded vessels, remains a two-to-three-month process.

US inflation data — not yet tested this week. No new CPI or PCE print landed in this window. The next reading remains the key test of whether the energy-driven component of inflation is washing out of the data the Fed is watching.

60-day Iran final-deal negotiation — first sign of fragility. Formal talks scheduled to take place in Switzerland were abruptly postponed on Friday, with no explanation given by either side. Brent ticked back up on the news — a reminder that the MoU is a framework, not a settled outcome, and that the follow-on negotiation on sanctions and nuclear terms remains unresolved.

Diamonds for Development Fund — still no board announcement. No independent board director news this week. The fund remains in its establishment phase pending the first board meeting under Adesina.

Spot gold rose as much as 1.7% this week to about $4,887 an ounce, its highest level since 17 March, after Iran declared the Strait of Hormuz completely open for commercial vessels during the ceasefire period. Silver surged over 5% to reach roughly $83 an ounce, a five-week high. With this move, bullion has now recovered more than half of its losses since the Middle East war began in February — the chain reaction flagged as the single highest-value catalyst for African mining finance, now visible in the price action rather than just the diplomatic announcement. Brent crude eased to around $80 a barrel — down sharply from its April peak above $120, though still roughly $20 above where it started the year. Separately, precious metals research firm Heraeus published an analysis building on the World Gold Council's central bank survey: gold now accounts for 27% of official reserve assets globally versus US Treasuries at 22%, and 75% of central banks that manage their gold reserves separately now view those reserves as a strategic asset, compared with only 44% a year ago. And a government-commissioned audit of First Quantum's shuttered Cobre Panama mine found it 88% compliant with its environmental, legal and operational obligations, keeping a potential restart of one of the world's largest copper mines on the table.

The chain reaction flagged as the single highest-value catalyst for African mining finance is now visible in market pricing, not just diplomatic announcements. Gold above $4,800, oil near $80, and silver at a five-week high all confirm the Hormuz reopening is feeding through faster than the cautious multi-month timeline outlined in the prior edition suggested it might. But Friday's abrupt postponement of the Switzerland talks is an important reminder: the underlying deal remains an interim framework, not a settled outcome, and the speed of this week's market recovery should not be mistaken for the speed at which the underlying political risk has actually been resolved.

Two themes stand out this week. The gold recovery scenario should be re-tested against current spot pricing, not held as a future case. With gold at $4,887, the $4,800–$5,000 medium-term recovery case outlined in the prior edition is no longer a forward-looking scenario — it is approximately where the market is trading today. AEMBank credit reviews for gold-exposed pipeline deals should re-run sensitivity analysis using current pricing as the new base case, while retaining the $4,000 downside scenario as a live possibility given Friday's reminder that the Iran deal remains an unsettled framework. Input cost relief for African copper and gold operations should still be modelled on a lag, not assumed from this week's price action — markets have moved faster than the physical supply chain, and the IEA's two-to-three-month normalisation timeline for Gulf shipping has not changed this week even though oil and gold prices have moved sharply.

Washington and Tehran signed a memorandum of understanding on Wednesday 17 June, formally ending military operations across the region and opening a 60-day window to negotiate a final deal. Oil fell below $80 per barrel for the first time since March — down from over $100 just weeks ago — triggering a chain reaction this newsletter has anticipated for months: lower oil, lower inflation pressure, less need for the Fed and ECB to keep hiking, easing acid and fuel costs for African miners, and a more supportive backdrop for gold. Gold itself had a volatile week, rising 3.6% to near $4,370 on the deal announcement before giving back most of that gain after Wednesday's hawkish FOMC meeting — Kevin Warsh's first as Chair. The World Gold Council's annual central bank survey, also released this week, supplies the structural counterweight to that volatility: 45% of central banks plan to add gold this year, a survey record, and 89% expect global official reserves to keep rising. Separately, the question of who controls Africa's mineral wealth sharpened on three fronts: Ghana is weighing whether to hand control of Gold Fields' flagship Tarkwa mine to local firms; Zimbabwe's government owes platinum producers $228 million in unpaid export earnings while its lithium miners ask for more time before a looming export ban; and Mike Teke told the Zimbabwe Chamber of Mines that Africa can no longer afford to negotiate its resource future country by country.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,630 – 1,690 | Continued weakness |

| ZAR — South African Rand | ~18.2 – 19.2 | Firmer on lower oil import bill |

| GHS — Ghanaian Cedi | ~15.0 – 16.0 | Weak; Tarkwa uncertainty an added factor |

| ZMW — Zambian Kwacha | ~25.3 – 26.6 | Stable to firmer on lower fuel costs |

| EUR — Euro | ~1.07 – 1.10 | Steady post-ECB hike |

| GBP — British Pound | ~1.30 – 1.34 | Broadly stable |

The US dollar pulled back from its post-CPI highs as the Iran deal reduced near-term inflation risk, before firming again on Wednesday's hawkish FOMC dot plot. South African and Zambian currencies both benefit marginally from lower oil import costs, though gains are partially offset by volatility in gold and PGM prices. Sources: LME, ICE, Refinitiv, CME, Fastmarkets.

Iran deal signature — delivered, but only as a framework. The variable flagged as the single most important watch point for seven consecutive weeks has materialised. Trump signed an MoU with Iran on Wednesday 17 June at the Palace of Versailles during the G7 summit, with a formal signing ceremony following in Geneva. The MoU declares the immediate and permanent termination of military operations across all fronts, including Lebanon, and commits both sides to negotiating a final deal within 60 days. Oil sanctions relief on Iran takes effect immediately.

Gold below $4,200 — reversed, then partially re-reversed. Gold's recovery on the Iran deal news was immediate and sharp, but gave back much of the gain after Wednesday's FOMC meeting confirmed a more hawkish rate path than markets had priced in. Net effect on the week: significant volatility, modest net change.

ECB September hike — still the base case. No new commentary this week that changes the picture. The lower oil price is the first concrete data point that could ease the inflationary pressure behind the ECB's hawkish posture — but one week is not enough to move a quarterly policy decision.

Diamonds for Development Fund — Adesina now in office, no board news yet. Adesina formally assumed his role as chairperson on 15 June as scheduled. No independent board director announcements have followed yet.

The single biggest geopolitical risk hanging over African mining finance since February formally began to resolve this week, even if the physical and economic effects will take months to fully materialise. Gold's volatile week shows the path from de-escalation to easier financing conditions is not instant — the Fed needs to see the inflation data turn before its own posture shifts — but the World Gold Council survey confirms the structural buyer base for gold remains larger and more committed than at any point in the survey's history. Meanwhile, the question of who controls Africa's mineral wealth is being contested simultaneously in Ghana, Zimbabwe, and on the conference stage in Victoria Falls. Ghana's government is weighing whether to transfer control of Gold Fields' Tarkwa mine — its largest single asset, producing 475,000 ounces in the most recent year — to local firms when its lease expires in April 2027, following the precedent set by the Damang mine earlier this year. Zimbabwe owes platinum producers $228 million in unpaid export earnings under its foreign currency retention system, while its lithium miners have asked for more time to build local processing plants ahead of a January 2027 concentrate export ban. And Seriti Resources CEO Mike Teke told the Zimbabwe Chamber of Mines conference that Africa can no longer afford fragmented voices on resource strategy.

The single biggest geopolitical risk hanging over African mining finance since February has formally begun to resolve this week, even if the physical and economic effects will take months to fully materialise. Lease renewal, currency conversion mechanisms, and continental coordination are no longer separate conversations — they are different fronts in the same underlying negotiation over who captures the value of Africa's minerals, and on what terms.

Three themes stand out this week. The Iran deal should be modelled as a phased recovery rather than a switch — AEMBank should build an explicit multi-month glide path into gold, copper and fuel-cost assumptions, with a near-term phase where physical normalisation lags the headline, and a medium-term phase where the full disinflationary effect should be visible if the 60-day negotiation succeeds. Gold sensitivity ranges should widen further in both directions — credit reviews should bracket current $4,200–$4,400 trading, a $4,000 downside if the Iran follow-on talks falter, and a $4,800–$5,000 medium-term case if both the deal holds and the Fed eases. Resource control risk needs to be explicitly underwritten alongside commodity and currency risk — Ghana's Tarkwa review, Zimbabwe's payment arrears, and the continental value-capture momentum collectively confirm that who controls an asset, and under what conversion and retention terms, is now a first-order credit consideration.

Gold fell below $4,200 on Wednesday 10 June — its lowest since January 2025 — after US May CPI printed at 4.2%, the highest since April 2023. The headline is almost entirely an energy story: core inflation rose just 0.2% for the month, meaning the inflation driving rate expectations is geopolitical, not structural. The European Central Bank raised rates for the first time since 2023, taking its deposit rate to 2.25% and citing the Iran war directly. US-Iran peace talks gathered real momentum through the week — copper rose 1.8%, gold recovered from its lows, oil eased on Friday before any signature. South Africa's Minerals Council reported R332 billion in mineral sales for January to April, up 36.5%, but sector fuel costs have nearly doubled. And the Invest Africa debate produced the sharpest reframing yet: processing without a buyer is not value capture — it is relocated risk.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,630 – 1,690 | Weakening |

| ZAR — South African Rand | ~18.4 – 19.4 | Volatile |

| GHS — Ghanaian Cedi | ~15.0 – 16.0 | Weak |

| ZMW — Zambian Kwacha | ~25.4 – 26.7 | Mild softening |

| EUR — Euro | ~1.07 – 1.10 | Firmer post-ECB hike |

| GBP — British Pound | ~1.30 – 1.34 | Broadly stable |

May CPI at 4.2% was overwhelmingly an energy story — core CPI rose just 0.2% for the month, with energy accounting for more than 60% of the monthly increase. This is a geopolitical shock, not demand-driven overheating. The ECB raised its deposit rate to 2.25% — its first hike since 2023 — cutting its 2026 eurozone growth forecast to 0.8%. Both the Fed and the ECB are now responding to the same root cause: a Middle East energy shock neither can address through rate policy. US-Iran peace negotiations intensified meaningfully through the week, with Trump suggesting a deal could be signed as early as 13–14 June. Markets moved before any signature — copper rose 1.8% Friday, gold recovered from its lows, Brent eased. The qualification remains: this is not the first time a deal has appeared imminent.

South Africa's mining sector is living the central tension of the year in real time: R332 billion in mineral sales for January–April 2026, up 36.5%, while average monthly fuel expenditure rose from R2.9 billion to R4 billion — a 38% increase driven directly by the Hormuz oil shock. PGM sector sales in March alone reached R25 billion, up 113.5% year on year. The Invest Africa debate in London on 8 June produced the most useful analytical reframing of the year: processing capacity without secured offtake is not value capture — it is relocated risk. The Ionic-AML offtake-first model validated this sequencing: secure the buyer before the capex.

Gold's decline is a geopolitical energy shock wearing an inflation headline — core CPI rose just 0.2%. The same Iran deal that could reverse gold's slide could ease acid supply, diesel costs and rate pressure simultaneously. Processing without a secured buyer is not value capture. It is relocated risk.

Three themes stand out. Gold project models need a wider sensitivity band in both directions — the $4,200 print reflects a specific identifiable driver that could reverse quickly; model three explicit scenarios: sub-$4,000 prolonged-conflict case, $4,200–$4,500 status-quo, and rapid recovery to $4,800–$5,000 on a verified Iran deal. European financing costs need explicit repricing — any transaction with European co-lenders or euro-denominated tranches should be re-quoted post-ECB hike, with a September follow-on as the working assumption. Beneficiation underwriting needs an offtake-first test — a project with capex committed ahead of secured offtake should be treated as carrying materially higher commercial risk than one with offtake secured first.

Gold erased all of its 2026 gains on Friday 5 June, falling to $4,319 — its lowest since 1 January — after the US economy added 172,000 jobs in May against a forecast of 85,000. Markets are now pricing a 63% probability of a Fed rate hike by December. Two competing answers to the question of what to do with African gold assets emerged in the same week: Barrick Mining is weighing a London listing for its African business with a potential merger with Endeavour Mining, while Zijin Mining received Canadian and African regulatory approval for its C$5.5 billion acquisition of Allied Gold. In Zambia, KCM reopened the Chingola B copper mine after 18 years — 200,000 tonnes of ore per month, 2.5% grade, a direct contribution to Zambia's 3 million tonne by 2031 ambition.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,630 – 1,690 | Weakening |

| ZAR — South African Rand | ~18.4 – 19.3 | Volatile |

| GHS — Ghanaian Cedi | ~15.0 – 16.0 | Weak |

| ZMW — Zambian Kwacha | ~25.4 – 26.7 | Mild softening |

| EUR — Euro | ~1.08 – 1.12 | Softening on strong dollar |

| GBP — British Pound | ~1.30 – 1.34 | Softening on strong dollar |

The US dollar strengthened sharply on Friday following the NFP report. ZAR came under particular pressure as South Africa's mining sector is acutely sensitive to the gold price. US 10-year Treasury yields rose above 4.50%.

Military strikes resumed on 1 June after Trump's 'largely negotiated' announcement proved premature. Brent fell toward $90/b amid peace optimism during the week before recovering above $100/b with the resumption of hostilities. The US economy added 172,000 nonfarm payroll jobs in May against a forecast of 85,000 — roughly double expectations. Gold's response was immediate: the metal fell more than 3% on the day, closing at $4,319 — its lowest since 1 January 2026 and below the level at which the year began. Markets are now pricing a 63% probability of a Fed rate hike by December 2026, up from approximately 45% the prior week.

The most important M&A week in African gold in years produced a clear split: Western capital is restructuring out of African political risk while Chinese capital is buying in. Barrick is weighing a London listing and potential merger with Endeavour Mining — a potential $30 billion African gold vehicle. Zijin received Canadian and African regulatory approval for its C$5.5 billion Allied Gold acquisition, though a 21% share price discount signals institutional scepticism about Chinese approval given Mali jurisdiction risk. Zambia's Chingola B copper mine reopened after 18 years — 200,000 tonnes per month at 2.5% grade, the most visible brownfield revival on the Copperbelt in the current cycle.

Gold's floor has broken. Western capital is restructuring out of African political risk; Chinese capital is buying in. The gap between those two positions is where the 21% Allied share price discount lives. Zambia's Chingola B reopening is the most concrete brownfield copper revival on the Copperbelt — a direct datapoint in the 3 million tonne ambition.

Gold's floor has moved and project models need to reflect it — a $4,000 to $4,200 scenario should be modelled explicitly alongside the structural recovery case. The Barrick-Allied divergence defines the M&A pricing environment: Western capital discounts African political risk; Chinese capital pays for African gold production. Projects that can demonstrate governance, permitting clarity and offtake structures that reduce political risk premiums will attract capital from both pools. Zambia copper brownfield revival is the most immediately bankable theme — Chingola B's reopening, Vedanta's investment commitment, and the partial restoration of acid supply collectively validate the investment environment.

Botswana and De Beers appointed former AfDB President Dr Akinwumi Adesina as inaugural chairperson of the Diamonds for Development Fund on 29 May — a fund seeded with $74 million and structured to channel diamond revenues directly into beneficiation and job creation. Sibanye-Stillwater reported Q1 EBITDA of $1.2 billion, up 371% year on year — the fourth consecutive set of extraordinary African mining earnings tracked in this newsletter. Ionic Rare Earths signed binding US defence supply agreements for its Uganda project, the same week China's rare earth enforcement deadline passed with no softening. And Zimbabwe formally codified its critical minerals strategy: 14 minerals classified as critical, raw exports banned, state co-ownership mandatory.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,620 – 1,680 | Weakening |

| ZAR — South African Rand | ~18.3 – 19.2 | Volatile |

| GHS — Ghanaian Cedi | ~14.9 – 15.9 | Weak |

| ZMW — Zambian Kwacha | ~25.3 – 26.6 | Mild softening |

| EUR — Euro | ~1.09 – 1.13 | Firm vs USD |

| GBP — British Pound | ~1.31 – 1.35 | Firm vs USD |

Brent crude fell on Iran deal optimism before recovering sharply as US and Iran resumed military strikes on 1 June. Weak Chinese manufacturing PMI of 50.0 in May added downward pressure across base metals.

Trump's 'largely negotiated' Iran announcement has not resulted in a signed agreement. Traffic through the Strait of Hormuz averaged seven ships per day — up from five the prior week, but still 95% below the pre-war level of 140. Gold closed at $4,513/oz — sixth consecutive week of decline — as hot US PCE and CPI data made rate cuts increasingly unlikely. Jinchuan Group confirmed $145 million siphoned from its DRC copper and cobalt operations through internal fraud — the same pattern reported in Nigeria two weeks earlier, now confirmed at the corporate level in the DRC. A direct due diligence signal for anyone financing DRC assets. China's 28 May rare earth enforcement deadline passed with no softening; November 2026 extraterritorial enforcement date remains in place.

Four weeks of extraordinary African mining earnings confirm that the commodity price environment is generating returns at a scale not seen in a decade. The Diamonds for Development Fund is the most concrete institutional expression of the African beneficiation thesis. Zimbabwe has written the most comprehensive critical minerals governance framework in southern Africa. Ionic Rare Earths' US defence supply agreement shows that African upstream assets are being formally integrated into Western ex-China supply chains — with Uganda at the leading edge.

Four weeks of extraordinary African mining earnings confirm that the commodity price environment is generating returns at a scale not seen in a decade. The geopolitical scramble for African minerals is no longer abstract — it is taking institutional form, week by week.

Three themes stand out. The four-week African earnings cycle establishes a new empirical pricing benchmark — four consecutive quarters of actual results demonstrate that disciplined African operations convert elevated commodity prices into debt-repaying free cash flow, supporting tighter spreads and longer tenors on well-structured transactions. The Diamonds for Development Fund opens a new co-financing dimension for beneficiation projects — projects that can position themselves as beneficiation investments are now more likely to attract fund co-investment alongside commercial lending. The Ionic-AML-Zimbabwe combination points to a new category of African project finance: sovereign-aligned critical minerals, where the offtake counterparty is a US government-aligned entity and structural protection is provided by both the sovereign mandate and the Western strategic procurement framework.

The Federal Open Market Committee minutes released on 21 May revealed deeper divisions inside the Federal Reserve than markets had expected, with four members dissenting — the highest count since 1992. A significant cohort still supports rate cuts if inflation moderates, directly sustaining the structural bull case for gold. Zambia partially lifted its sulphuric acid export ban, authorising two smelters to resume limited shipments to the DRC — the first easing in a supply crisis tracked for months. Nedbank arranged a $700 million project financing for Ivanhoe's Platreef platinum mine in South Africa — the largest African mining project finance deal in a decade. And Tharisa reported profit after tax up 468%, continuing the pattern of extraordinary African mining earnings across the past three weeks.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,620 – 1,680 | Weakening |

| ZAR — South African Rand | ~18.3 – 19.2 | Volatile |

| GHS — Ghanaian Cedi | ~14.9 – 15.9 | Weak |

| ZMW — Zambian Kwacha | ~25.3 – 26.6 | Mild softening |

| EUR — Euro | ~1.09 – 1.13 | Firm vs USD |

| GBP — British Pound | ~1.31 – 1.35 | Firm vs USD |

NGN and GHS continued to weaken, compounding USD-denominated cost pressures for African miners. The Indian rupee remained at an all-time low — the underlying driver of India's silver import restrictions.

The FOMC minutes delivered more clarity on the Fed's internal state than the headline vote suggested — three distinct camps emerged, with four dissents recording the highest count since 1992. Gold and silver recovered mid-week as markets focused on the sizeable dovish cohort. Brent crude fell on Trump's 'largely negotiated' Iran announcement before recovering on contradictory Iranian signals — confirming the Hormuz situation remains the single most consequential variable for every commodity. South Africa's mining production for March 2026 rose 10.2% month on month and 2.5% year on year, with precious metals, chrome, manganese and nickel all increasing. Zambia partially lifted its sulphuric acid export ban — the first easing since the crisis began — though volumes remain capped and Mopani's permit was reportedly not yet physically received at time of reporting.

The Federal Reserve's internal division is the most constructive macro signal gold has received in weeks — the majority still wants to cut and is being held back by a specific temporary shock, not a structural reversal. The Zambia acid partial lift is the first positive supply chain signal from the Copperbelt in months. Nedbank's $700 million Platreef financing confirms African mining project finance is operating at scale, led by African institutions. The DRC-US cobalt MoU and Appian's Namibia copper commitment both signal that international capital is actively positioning for African minerals — not waiting.

The Federal Reserve's majority still wants to cut rates. Zambia's acid ban is partially lifting. Nedbank just closed the largest African mining project finance deal in a decade. The structural case for African minerals is being confirmed deal by deal — the question is whether the macro headwinds ease fast enough for the window to remain open.

Three themes stand out this week. The Platreef transaction defines what bankable African mining looks like in the current cycle — a three-institution syndicate combining domestic expertise, regulatory knowledge and international capital market access, applied to a polymetallic asset with diversified cash flows. The FOMC division is a timing signal, not a directional reversal — the committee's majority still supports rate cuts and the current rate environment should be modelled as the ceiling, not a permanent floor. The DRC cobalt MoU and Zambia acid resumption signal that the Copperbelt corridor is becoming a focal point for structured supply chain financing, with US government-aligned strategic buyers now emerging as a new category of offtake counterparty.

Copper hit an all-time record above $14,000 per tonne on 12 May before giving back the gains as the Trump-Xi summit disappointed markets and Chinese economic data came in weak. Goldman Sachs revealed its gold demand model had been underestimating central bank purchases by more than 70% since August 2025 — revised figures show buying is running at nearly double previously reported levels, materially changing the recovery story for gold. India, the world's largest silver buyer, restricted most silver imports on 16 May to defend a weakening rupee, creating a near-term supply dislocation in precious metals markets. And a joint Nigerian government report confirmed that foreign buyers are extracting mineral value from the country before it ever enters the formal economy.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,610 – 1,670 | Weakening |

| ZAR — South African Rand | ~18.2 – 19.0 | Volatile |

| GHS — Ghanaian Cedi | ~14.8 – 15.8 | Weakening |

| ZMW — Zambian Kwacha | ~25.2 – 26.5 | Mild softening |

| INR — Indian Rupee | ~95.4 – 96.5 | All-time low |

| EUR — Euro | ~1.09 – 1.13 | Firm vs USD |

| GBP — British Pound | ~1.31 – 1.35 | Firm vs USD |

NGN and GHS continued to weaken, adding to USD-denominated cost pressures for African miners. The Indian rupee reached an all-time low — the direct trigger for India's silver import restriction announced on 16 May.

Copper's all-time high of $14,527.50/t on the LME on 12 May was driven by African supply declines — Zambia's copper output fell 4.27% and DRC copper exports fell nearly 15% in Q1, with the sulphuric acid crisis a direct cause. The retreat came when the Trump-Xi summit ended without trade concessions and Chinese retail sales and industrial production both missed expectations. Gold declined for a fourth consecutive week — now down approximately 16% from its January all-time high of $5,589 — as rising real yields, a rebounding dollar, and rate-hike expectations weighed on the metal. However, Goldman Sachs revised its central bank buying model upward by over 72%, reframing the decline as a macro-driven correction rather than a demand reversal.

Copper hit an all-time record and the acid shortage is cutting actual production from Africa's two largest copper producers simultaneously — that is a supply squeeze made visible. The Goldman gold revision shows the structural buyer base has been larger than anyone expected. And the Nigeria report captures the central failure of African mining at scale: wealth in the ground is not the same as wealth in the economy when extraction is dominated by foreign intermediaries operating outside the formal system.

Copper hit an all-time record this week while Africa's two largest producers are simultaneously cutting output. Gold's structural buyer base is 70% larger than markets had priced. The gap between Africa's mineral endowment and the value that stays on the continent has never been more visible — or more urgent to close.

Three themes stand out this week. The copper supply story has moved from forecast to real-time — Zambia and DRC are producing less copper, and the acid shortage means this will not self-correct quickly. The Goldman gold revision resets the baseline assumption — central bank buying has been more robust than reflected in traded prices, supporting a view that current price weakness is cyclical not structural. The Nigeria report is a due diligence signal — it identifies shell companies, local proxies, misinvoiced exports and cash-based transactions as dominant elements of the trade infrastructure, providing a detailed map of the risks that must be addressed before capital can be deployed.

Two landmark earnings results this week illustrate the scale of returns that elevated precious metal prices are generating. AngloGold Ashanti reported record free cash flow of $1.2 billion — almost tripling year on year — from African gold operations. Wheaton Precious Metals posted record revenue of $901 million with net earnings up 129%. At the same time, Australia and Japan signed a A$1.3 billion critical minerals deal, signalling that allied countries are now building independent supply chains without China or the US. Africa holds the minerals at the centre of all of these developments.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,590 – 1,650 | Weak |

| ZAR — South African Rand | ~18.0 – 18.8 | Volatile |

| GHS — Ghanaian Cedi | ~14.6 – 15.5 | Weakening |

| ZMW — Zambian Kwacha | ~25.0 – 26.2 | Stable |

| EUR — Euro | ~1.09 – 1.12 | Firm vs USD |

| GBP — British Pound | ~1.31 – 1.34 | Firm vs USD |

NGN and GHS continued to weaken against the dollar, adding to import cost pressures for African miners. ZMW held relatively stable.

Brent crude pulled back to $103–$112/bbl on reports of new Iranian peace proposals, providing partial relief on energy costs. Gold declined for a third consecutive week as rate-hike expectations driven by energy-led inflation continued to weigh on the metal — now down approximately 15% from its January high of $5,595/oz. Despite price weakness, Q1 earnings confirmed the gold price environment of the past twelve months has been transformative for African producers. Copper continued to find support from supply tightness, with China's sulphuric acid export halt still in effect. The Australia-Japan critical minerals agreement confirmed that allied nations are actively locking in supply of materials — graphite, nickel, rare earths and fluorite — all of which Africa holds in significant quantities.

The earnings results this week tell a consistent story: elevated commodity prices are generating returns at a scale African producers have not seen before. AngloGold tripled its free cash flow. Wheaton posted record revenue of $901 million. Both results reflect the same dynamic — high prices meeting disciplined operations. At the same time, the Australia-Japan deal shows the geopolitical scramble for the minerals Africa holds is intensifying. The question is whether African producers and governments can use this window to negotiate better terms before alternative supply chains elsewhere become more developed.

African gold assets — managed with cost discipline — can generate returns that repay debt, fund growth and return capital to shareholders simultaneously. The question is not whether the assets can perform. It is whether the right financing structures are in place to capture that performance.

Three financing themes emerge clearly this week. High commodity prices are generating transformative results for African producers — AngloGold's balance sheet swing from $755 million net debt to $868 million net cash in twelve months illustrates the leverage that sustained high gold prices deliver. Streaming is proving its value and the appetite for new agreements is active — Wheaton completed a $4.3 billion transaction with BHP and holds $2.16 billion in cash ready to deploy. The geopolitical scramble for minerals is creating new financing entry points — the Australia-Japan deal and broader bilateral mineral agreements signal that government-backed financing is increasingly available for projects in trusted supply chains.

Three converging developments reinforced Africa's central position in global critical mineral supply chains this week. Glencore's Q1 results showed DRC government policy already redirecting output — copper up 19%, cobalt down 39%. China tightened its rare earth enforcement framework while its sulphuric acid export halt took effect, placing simultaneous pressure on copper processing across the DRC, Zambia and Chile. Against this backdrop, a new forecast of a near-decade lithium supply deficit points to a structural opportunity for Africa — provided the financing and infrastructure to unlock it moves quickly.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,580 – 1,640 | Weak |

| ZAR — South African Rand | ~18.2 – 19.0 | Volatile |

| GHS — Ghanaian Cedi | ~14.5 – 15.4 | Weakening |

| ZMW — Zambian Kwacha | ~25.2 – 26.5 | Stable |

| EUR — Euro | ~1.08 – 1.11 | Firm vs USD |

| GBP — British Pound | ~1.30 – 1.34 | Firm vs USD |

NGN and GHS continued to weaken against the dollar, adding to import cost pressures for African miners. The ZMW held relatively stable.

China-linked supply risks intensified, with several policy actions moving from signal to implementation. The sulphuric acid export halt took effect on 1 May — acid prices in Chile have already risen 44%, and the supply impact on SX-EW copper operations in the DRC and Zambia is now live, not forecast. China's rare earth export restrictions have been followed by tighter domestic enforcement, with Beijing tightening control from both ends: export controls at the border and quota enforcement at the mine. Gold's pullback has developed into a clearer downward trend, now down approximately 15% from its January high of $5,595/oz, as the safe-haven thesis is tested by renewed rate-hike expectations driven by energy-led inflation. Lithium pricing has strengthened in direction, with Canaccord's deficit forecast pointing to an emerging price floor with the supply gap appearing more structural than cyclical.

Glencore is already pivoting its African operations in response to DRC government policy. China is locking down rare earth production with the most detailed enforcement system it has ever built. And the lithium market is heading into a supply deficit that could last close to a decade — with Africa holding the reserves the world needs but lacking the financing and infrastructure to unlock them at speed. The minerals are there. The demand is real and growing. The question is who moves fast enough to connect the two.

The minerals are there. The demand is real and growing. The question is who moves fast enough to connect the two — and whether African governments negotiate the terms that keep value on the continent.

This week's developments reinforce a shift in what determines whether a mining project moves forward in Africa. The question is no longer simply whether capital is available — it is whether projects can demonstrate cost resilience, input supply security, and deal structures that work for both investors and host governments. The sulphuric acid situation is worth watching closely: if the shortage persists, it could affect output at some African copper operations and push production costs higher across the region.

The week of 20–24 April was shaped by two converging pressures: the continued impact of the Middle East conflict on energy and input costs, and growing recognition that Africa's position in global critical mineral supply chains is strengthening at a time when the continent's ability to capture that value remains constrained. Gold softened to around $4,713/oz — down roughly 3% on the week — as rising energy costs fuelled inflation concerns and raised questions about the interest rate outlook. A partial recovery emerged on Friday on reports of potential US-Iran peace talks. The structural case for gold remains intact, with central bank demand continuing to provide a floor and year-end forecasts of $5,055/oz unchanged.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,560 – 1,620 | Weak |

| ZAR — South African Rand | ~18.4 – 19.5 | Volatile |

| GHS — Ghanaian Cedi | ~14.2 – 15.1 | Weakening |

| ZMW — Zambian Kwacha | ~25.0 – 26.8 | Stable |

| EUR — Euro | ~1.07 – 1.10 | Firm vs USD |

| GBP — British Pound | ~1.29 – 1.33 | Firm vs USD |

NGN and GHS continued to weaken against the dollar, adding to import cost pressures for African miners. The ZMW held relatively stable.

The partial closure of the Strait of Hormuz is having a direct effect on mining input costs globally — diesel and sulphuric acid supply are both affected, with commodity prices forecast to rise 16% in 2026 as a result of the energy shock. For Africa, higher import costs are adding to existing FX pressures, with regional growth projected to slow by up to 0.2 percentage points. Copper held above $13,200/t, supported by Chinese restocking ahead of the May Day holiday and record refined copper output of 1.33 million tonnes in March. However, China's decision to halt sulphuric acid exports from May — combined with the Hormuz-driven sulphur shortage — is placing simultaneous pressure on copper processing capacity in the DRC, Zambia, and Chile.

Africa's strategic importance in global mineral supply chains continued to grow this week, reflected in BHP's active engagement across southern Africa and the strengthening of US critical minerals policy. At the same time, rising input costs and the sulphuric acid supply squeeze are creating real near-term pressure for producers in the DRC and Zambia.

Capital structuring — not capital availability — remains the defining factor in which projects get built. The question is no longer simply whether capital is available, but whether projects can demonstrate cost resilience, input supply security, and deal structures that work for both investors and host governments.

Africa holds approximately 20% of global mineral wealth — an estimated $29.5 trillion in mine-site value, of which $8.6 trillion remains undeveloped — yet the continent accounts for only 3% of global manufacturing output. Projected demand growth to 2050 reinforces why this matters: up to 66x for PGMs, 29x for manganese, 13x for lithium, and 5x for graphite. Four broad approaches are being debated:

Rising costs are narrowing margins across the sector. Even where commodity prices are high, producers are seeing costs climb due to fuel price increases and supply chain disruption. For African projects, where fuel is typically imported and currencies are weaker, this pressure is felt more directly. The sulphuric acid situation is worth watching closely — if the shortage persists, it could affect output at some African copper operations and push production costs higher across the region.

Gold prices continued their steady upward trend this week, reinforcing momentum across Africa's gold sector as prices remain near recent highs. Geopolitical tensions — particularly in the Middle East — continue to drive safe-haven demand, with investors and central banks increasingly turning to gold as a stable reserve asset. Oil prices softened slightly over the week, suggesting some easing in immediate supply concerns. Elevated copper prices continue to reflect tightening supply conditions and strong structural demand linked to electrification and infrastructure.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,340 – 1,400 | Weak |

| ZAR — South African Rand | ~18.0 – 19.2 | Volatile |

| GHS — Ghanaian Cedi | ~13.5 – 14.8 | Weakening |

| ZMW — Zambian Kwacha | ~24.5 – 26.5 | Stable |

| EUR — Euro | ~1.06 – 1.09 | Firm vs USD |

| GBP — British Pound | ~1.30 – 1.34 | Firm vs USD |

Ongoing tensions in the Middle East are beginning to impact global economies more broadly. A joint policy document presented by the African Union Commission, African Development Bank Group, UNECA, and UNDP forecasts that growth across African countries could decline by up to 0.2 percentage points, largely due to higher energy prices, rising import costs, and increased pressure on fiscal balances. Despite this, gold's safe-haven appeal continues to strengthen, with central banks and investors turning to it as a stable reserve asset.

Africa's gold sector is gaining renewed momentum, supported by sustained high prices and strong global demand. The development of pilot gold refining capacity in the DRC signals a broader shift toward capturing more value locally. The pace of translating this momentum into production, however, continues to depend on financing, infrastructure, and execution capacity.

Capital structuring — rather than capital availability — is increasingly determining which projects move forward. The Cora Gold streaming deal signals a maturing market where execution-ready projects can access funding on competitive terms.

The Cora Gold transaction illustrates the growing use of streaming agreements, where upfront funding is secured in exchange for future production at discounted prices. This allows companies to advance projects without taking on traditional debt or diluting equity — a structure becoming increasingly relevant for African mining projects where access to conventional financing remains constrained.

This week's developments highlight two key structural shifts shaping global mining markets. Central banks — particularly among BRICS+ countries — continue to increase gold reserves, now exceeding 6,000 tonnes, reflecting a broader shift toward reserve diversification and reduced reliance on the US dollar. Rare earth supply chains remain highly concentrated, with China maintaining dominance across both mining and refining. Together, these trends reinforce the increasing strategic importance of both gold and critical minerals within global financial and industrial systems.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,500 – 1,650 | Weak |

| ZAR — South African Rand | ~18.5 – 19.8 | Volatile |

| GHS — Ghanaian Cedi | ~14 – 15.5 | Weakening |

| ZMW — Zambian Kwacha | ~25 – 27 | Stable |

| EUR — Euro | ~1.07 – 1.10 | Firm vs USD |

| GBP — British Pound | ~1.30 – 1.34 | Firm vs USD |

Central banks — particularly among BRICS+ countries — continue to increase gold reserves, now exceeding 6,000 tonnes, reflecting a broader move toward reserve diversification and reduced reliance on the US dollar. Meanwhile, rare earth supply chains remain highly concentrated, with China maintaining dominance across both mining and refining. While global demand continues to grow, the development of alternative supply chains is being slowed by financing constraints and project risk.

Africa's strategic importance continues to strengthen, but the pace at which this translates into investment and production is increasingly dependent on financing, infrastructure, and execution capacity.

Africa's strategic importance continues to strengthen, but the pace at which this translates into investment and production is increasingly dependent on financing, infrastructure, and execution capacity.

The current environment highlights a growing shift in how mining projects are financed. Rare earth supply chains illustrate that the key constraint is increasingly financing rather than resource availability — high project risk, long development timelines, and price volatility continue to limit access to capital. Transactions such as the IDC's equity participation in the Prieska project demonstrate how development finance institutions are using capital structuring to de-risk projects and unlock investment.

Global mining markets this week were shaped by moderating geopolitical tensions, sustained energy price sensitivity, and intensifying competition for critical minerals. Brent crude remained elevated around $100/bbl despite slight easing, reflecting persistent supply-side risks. Gold strengthened on renewed safe-haven demand, while copper stabilised following recent declines, supported by strong long-term fundamentals linked to electrification and industrial expansion. For Africa, cost pressures remain elevated, but the continent's strategic importance continues to strengthen as global players intensify efforts to secure diversified mineral supply chains.

This week reflected partial market stabilisation following prior volatility, with commodity-specific trends shaping investor positioning.

While immediate tensions in the Middle East showed signs of easing, underlying risks remain, particularly around energy security and global trade alignment. This is reinforcing copper, cobalt, lithium, and rare earths as strategic assets, while gold continues to reflect safe-haven positioning in uncertain markets.

Current dynamics present both opportunity and threat for African mining. Continued global supply chain diversification is increasing demand for African mineral assets, particularly in copper, cobalt, and other transition metals. Strategic corridors and production expansion targets across Zambia and the DRC continue to attract long-term capital.

Africa's position in global supply chains continues to deepen, but capital is becoming more disciplined — favouring well-structured, bankable projects over early-stage exposure.

| Currency | Range (vs USD) | Trend |

|---|---|---|

| NGN — Nigerian Naira | ~1,500 – 1,650 | Weak |

| ZAR — South African Rand | ~18.5 – 19.8 | Volatile |

| GHS — Ghanaian Cedi | ~14 – 15.5 | Weakening |

| ZMW — Zambian Kwacha | ~25 – 27 | Stable |

| EUR — Euro | ~1.07 – 1.10 | Firm vs USD |

| GBP — British Pound | ~1.30 – 1.34 | Firm vs USD |

Weaker currencies support USD revenues but increase import and financing costs, while volatility continues to complicate project planning and capital structuring.

Continued policy alignment toward expanding copper production and attracting long-term investment.

Ongoing focus on maximising value from critical mineral resources across the value chain.

Continued FX and fiscal reforms aimed at improving investor confidence and project viability.

The current environment presents both risks and opportunities for financiers. Recent transactions — including the IDC's conversion of debt into equity in Orion Minerals' Prieska project — highlight a growing trend of development finance institutions taking strategic equity positions to de-risk projects and catalyse private capital participation.